Indonesia is accelerating plans to establish its first national cryptocurrency exchange, with the launch anticipated in the upcoming weeks, as confirmed by the country’s Commodity Futures Trading Supervisory Agency (CFTRA), also known as Bappebti.

Bappebti intends to inaugurate the exchange in July 2023, as reported by local media outlet Tempo. According to Bappebti’s head, Didid Noordiatmoko, the national exchange will be the exclusive platform for cryptocurrency transactions in Indonesia.

The final rules for the stock exchange have been agreed upon, and procedures for customer identification, known as Know Your Customer (KYC) norms, have been part of the discussions.

The CFTRA has tested an integrated application that would facilitate transactions on the exchange. A recent system integration test between traders, exchanges, clearing, and depository has been successfully conducted, according to Noordiatmoko.

Bappebti’s strategy is to restrict the sale of cryptocurrencies to local transactions while keeping pace with global market trends.

READ MORE: Robert F. Kennedy Jr. Pledges to Back US Dollar with Bitcoin if Elected President

This includes Bappebti-sanctioned cryptocurrency pricing.

Trade Minister Zulkifli Hasan has been updated on the project’s progress. Unless further instructions are received, Bappebti will authorize the permit, allowing licensed traders a month to register with the exchange.

The plan to launch the national cryptocurrency exchange dates back to 2021, beginning as a collaboration between state-backed telecom firm owners and Binance, a major global cryptocurrency exchange. Binance upped its stake in the Indonesian crypto asset trader Tokocrypto in late 2022.

While the original launch target was December 2022, later moved to June 2023, delays have pushed the debut to July 2023.

Other Stories:

Why You Should Be Bullish Despite Bitcoin Price Falling Below $30,000

Bitcoin Mining Companies Employ Derisking Strategies, Offload BTC to Exchanges

The United States Department of Justice (DoJ) recently filed a complaint against Sam Bankman-Fried (SBF), the founder of FTX, alleging that he leaked private documents belonging to Caroline Ellison, who was previously both his business ally and romantic partner.

According to the complaint filed on July 20, the DoJ claims that Bankman-Fried attempted to interfere with a fair trial by publicly discrediting Ellison, who had become a government witness in SBF’s case in late 2022.

The accusation is based on Bankman-Fried’s act of sharing Ellison’s personal writings with a reporter, resulting in the publication of an article by The New York Times on July 20.

The U.S. Attorney Damian Williams argued that SBF aimed to discredit the government witness by featuring her private documents in the article.

The DoJ does not explicitly name the source of the leaked documents in the article, but Williams asserts that it is apparent that Bankman-Fried was responsible for sharing them.

Defense counsel confirmed that SBF had met with one of the article’s authors in person and provided documents that were not part of the government’s discovery material.

Williams highlights that these documents seem to have originated from Bankman-Fried’s personal Google Drive account and were not part of the case’s discovery materials.

He emphasizes that releasing non-public information that could interfere with a fair trial is prohibited by U.S. federal rules of civil procedure.

The government requests the court to enter an order, pursuant to Local Rule 23.1, which prohibits extrajudicial statements by parties and witnesses likely to affect the right to a fair trial by an impartial jury.

Williams stresses that having the article published in a reputable newspaper without identifying the defendant as the source misleads readers and compounds the risk of tainting prospective jurors.

As of now, both the DoJ and SBF’s defense attorneys have not responded to media inquiries about the complaint.

FTX, once a major global cryptocurrency exchange, experienced a collapse in mid-November 2022, possibly due to the liquidity crisis of the company’s FTT token and the 2022 bear market.

The link between FTX and Alameda was also cited as a contributing factor to the collapse.

Following the implosion of his crypto empire, Bankman-Fried faced seven lawsuits by early December 2022.

He is scheduled to appear in court on October 2 to address multiple charges, including fraud, illegal political donations, and bribes to the Chinese government.

Other Stories:

Why You Should Be Bullish Despite Bitcoin Price Falling Below $30,000

Bitcoin Mining Companies Employ Derisking Strategies, Offload BTC to Exchanges

Robert F. Kennedy Jr. Pledges to Back US Dollar with Bitcoin if Elected President

Web3 crime is undergoing a significant shift away from Bitcoin (BTC) towards stablecoins, and Ponzi schemes continue to plague the cryptocurrency landscape, according to Tara Annison, former head of technical crypto advisory at Elliptic.

During her presentation at EthCC in Paris, Annison shed light on the various ways digital assets are being exploited for criminal activities or money laundering.

Drawing insights from Elliptic, Chainalysis, and TRM Labs, Annison, as a former Elliptic employee, emphasized that the days of Bitcoin being the go-to choice for illicit activities are over.

As the crypto industry has matured, decentralized finance protocols, mixing services, and stablecoins have opened up new opportunities for criminals.

Dollar-denominated assets like USD Coin (USDC) have become the preferred choice due to their ease of access and potential to be laundered through decentralized exchanges (DEXs).

Criminals target these assets because of their deep liquidity and substantial volume, making it relatively easy to obscure their activities.

However, Annison pointed out a potential positive aspect for law enforcement, noting that centralized issuers like Circle can freeze specific USDC tokens before criminals can convert them to fiat through DEXs or centralized exchanges, effectively blocking their access to the funds.

Ponzi and pyramid schemes continue to be a problem in the sector, with criminals having stolen a staggering $7.8 billion from unsuspecting victims through these scams.

Moreover, criminals have become more sophisticated in their money laundering techniques, resorting to chain swapping and asset swapping to evade detection by blockchain analytics firms, amounting to around $4.1 billion in laundered funds.

Interestingly, despite the prevalence of scams, the sector has seen a decline of 46% in scam-related activities compared to previous years.

Annison attributes this to the ongoing bear market, which has made the sector less attractive for cybercriminals due to decreased hype and lower cryptocurrency prices.

Annison also brought attention to the increasing misuse of cryptocurrencies to evade sanctions and finance terrorist activities, highlighting popular assets like TRON (TRX) and Tether (USDT) being used for illicit purposes.

The rise of metaverse experiences has also attracted criminal actors, with various crimes emerging in virtual worlds, including phishing attacks, non-fungible token theft, wallet tampering, and augmented reality hacks.

In conclusion, Annison’s presentation highlighted the reality of criminal activity in the Web3 sector, signaling the need for heightened security measures to protect users and combat illicit activities effectively.

As the landscape continues to evolve, staying vigilant and implementing robust security protocols will be crucial in safeguarding the digital asset ecosystem.

Other Stories:

Why You Should Be Bullish Despite Bitcoin Price Falling Below $30,000

Bitcoin Mining Companies Employ Derisking Strategies, Offload BTC to Exchanges

Robert F. Kennedy Jr. Pledges to Back US Dollar with Bitcoin if Elected President

The Royal Canadian Mounted Police (RCMP) in Richmond, located south of Vancouver, has issued a public warning about a concerning trend involving cryptocurrency investors falling victim to home robberies.

Over the past year, several similar incidents have been reported, prompting the RCMP to address the matter for public safety.

According to Staff Sergeant Gene Hsieh of the Richmond RCMP Major Crime Unit, the criminals behind these robberies are deliberately targeting high-value cryptocurrency investors.

In each case, the perpetrators have posed as delivery drivers to gain access to the victims’ homes. Once inside, they rob the victims of information that grants them access to their cryptocurrency accounts.

Staff Sergeant Jill Long of the Delta Police Investigative Services added that the suspects appear to have extensive knowledge about the victims’ cryptocurrency investments and their residential locations.

This suggests that the criminals are specifically targeting individuals who are heavily invested in cryptocurrencies.

While the RCMP has made one arrest in connection with these incidents, they have not confirmed whether multiple robberies are linked.

Due to ongoing investigations, specific details about the number of incidents and the amount of stolen cryptocurrency have not been disclosed.

READ MORE: Bitcoin Mining Companies Employ Derisking Strategies, Offload BTC to Exchanges

To prevent falling victim to such home robberies, the police department offered valuable safety advice.

They urge homeowners not to allow strangers or even seemingly legitimate delivery personnel into their homes.

Instead, all deliveries should be left outside, and if there is any doubt about the person’s identity, homeowners are encouraged to contact the delivery company for verification.

In cases where danger seems imminent, authorities should be notified immediately.

The RCMP also advised storing valuables and financial information securely within the household, such as in a safe or safety deposit box.

Additionally, they emphasized the importance of discussing financial matters in private, rather than on social media, and only with trusted individuals.

The warning comes after a previous incident in which a Canadian cryptocurrency investor, known as the “Crypto King,” was allegedly kidnapped, falsely imprisoned, and assaulted by five men involved in a cryptocurrency scheme.

One of the suspects, who invested a significant amount of money in the scheme, was charged with kidnapping the investor.

In light of these recent occurrences, the RCMP is urging cryptocurrency investors to exercise extreme caution and implement additional security measures to safeguard their assets and personal safety.

As the investigations continue, law enforcement authorities are working diligently to apprehend those responsible for these targeted robberies and ensure the protection of the public.

Other Stories:

Why You Should Be Bullish Despite Bitcoin Price Falling Below $30,000

Robert F. Kennedy Jr. Pledges to Back US Dollar with Bitcoin if Elected President

Chainlink Labs, the development firm behind the Chainlink protocol and its native token, LINK, has introduced its cross-chain protocol to facilitate interoperability between traditional financial institutions and public and private blockchains.

In a recent blog post on July 17, Kemal El Moujahid, the Chief Product Officer of Chainlink Labs, announced the launch of the Cross-Chain Interoperability Protocol (CCIP) on Ethereum, Avalanche, Polygon, Arbitrum, and Optimism. Starting July 20, developers on these platforms will be able to access CCIP on their respective testnets.

CCIP is an interoperability protocol designed to enable enterprises to transfer data and value directly between public or private blockchain environments from their backend systems.

Chainlink’s solution for interoperability leverages Swift’s messaging infrastructure, which is widely used by more than 11,000 banks globally to facilitate international payments and settlements.

In 2021 alone, the network processed approximately $1.8 quadrillion in transactions from its 11,000 member banks, as reported by the United States Financial Crimes Enforcement Network.

Sergey Nazarov, the co-founder and CEO of Chainlink, explained that CCIP aims to bridge the gap between the on-chain and off-chain worlds, much like TCP/IP transformed the fragmented early internet into the unified global internet we know today.

READ MORE: Web3 Needs Asset Protection, and This Startup Wants to Make it Widely Available

Nazarov emphasized that an interoperability solution capable of seamlessly transmitting value between networks is a crucial foundation for a blockchain-powered society.

Several notable financial institutions, including BNY Mellon, BNP Paribas, Citi, Australia and New Zealand Banking Group, Clearstream, Euroclear, and Lloyds Banking Group, are exploring the use of Chainlink’s interoperability solution, according to the company.

Aside from the integration of CCIP with five blockchains, the decentralized finance protocol AAVE plans to implement the interoperability solution, while the decentralized derivatives platform Synthetix is already live on the CCIP mainnet.

Following the launch of CCIP on the mainnet, the price of Chainlink’s LINK token experienced a 9.7% surge in the previous eight hours, reaching $7.27, while the rest of the market remained relatively stable, according to CoinGecko.

Cointelegraph contacted Chainlink Labs for further comment but did not receive an immediate response.

Other Stories:

Ex-Federal Prosecutor Surprised by Potential SEC Appeal in Ripple Case

3 Best Crypto PR Agencies – Fees, Results and Full Review

Bitcoin On-Chain Data Reveals $30,000 as Most Popular ‘Buy’ Level

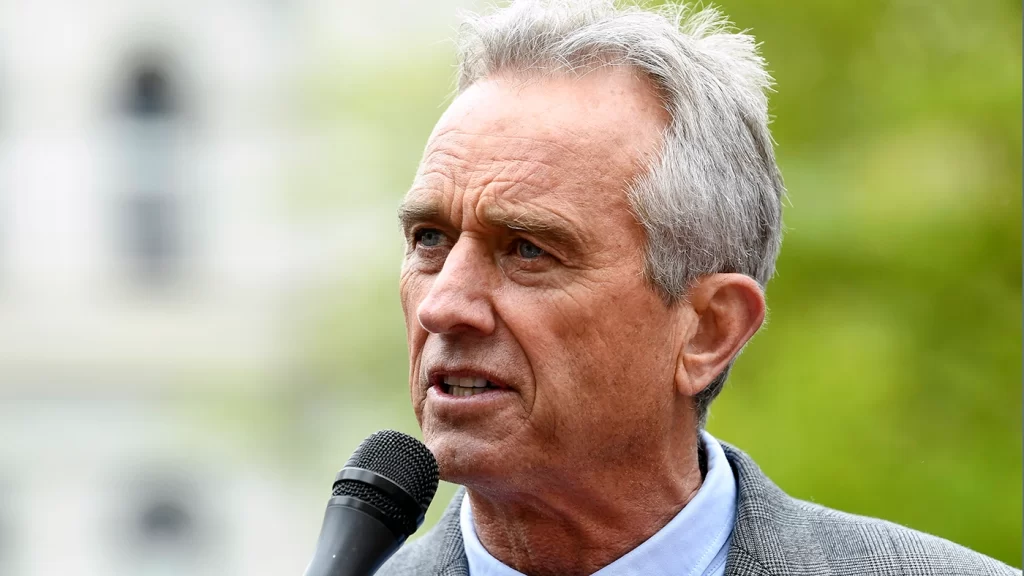

Democratic presidential candidate Robert F. Kennedy Jr. has unveiled his plan to back the United States dollar with Bitcoin (BTC) if he wins the presidency.

Kennedy made this announcement during a Heal-the-Divide PAC event on July 19, where he emphasized the potential of using “hard currency” like gold, silver, platinum, or Bitcoin to stabilize the American economy.

Kennedy believes that backing the U.S. dollar with tangible assets could strengthen the currency, combat inflation, and foster financial stability, peace, and prosperity in the nation.

He clarified that this process would be implemented gradually, and the level of backing for the dollar would be adjusted based on the success of the plan.

To initiate the strategy, Kennedy proposed a conservative approach, suggesting that initially, only a small portion of issued T-bills, perhaps around 1%, would be backed by hard currency such as gold, silver, platinum, or Bitcoin.

In addition to his backing of Bitcoin, Kennedy also declared his intention to exempt Bitcoin to U.S. dollar conversions from capital gains taxes.

READ MORE: Celo Blockchain Plans Transition to Ethereum Layer-2 Solution

He believes that this exemption would encourage investment and incentivize businesses to choose the United States as their primary location, rather than crypto-friendly jurisdictions like Singapore or Switzerland.

Kennedy’s recent statements in support of Bitcoin follow his participation in the Bitcoin 2023 conference in Miami on May 19, where he announced that he would accept political campaign donations in Bitcoin.

Surprisingly, investment disclosures on July 9 revealed that Kennedy himself owned up to $250,000 worth of Bitcoin, contradicting his earlier claims of having no exposure to the asset.

Kennedy is not the only presidential candidate making promises related to cryptocurrencies.

On July 14, Republican presidential candidate and Florida Governor Ron DeSantis vowed to ban central bank digital currencies if elected as president, asserting that such currencies would have no place in the United States under his leadership.

As the race for the presidency continues, it remains to be seen how these crypto-based promises and proposals will shape the future of the American economy and financial landscape.

Other Stories:

PEPE Coin in Trouble? Financial Regulator Clamps Down On Crypto Memes

SEC Chair Gary Gensler Advocates Greater Use of Artificial Intelligence for Market Surveillance

FSB Proposes Global Regulatory Framework for Cryptocurrencies

According to a market report from Bitfinex, Bitcoin (BTC) mining companies are adopting derisking strategies by selling BTC to exchanges.

The report highlights a recent surge in miners offloading large volumes of BTC to exchanges, resulting in an increase in the value of shares in Bitcoin mining companies. Institutional interest in BTC is also growing in 2023.

The report points out that Poolin has been responsible for the highest amount of BTC sold in recent weeks. Bitfinex analysts note that the Bitcoin mining difficulty recently reached an all-time high, which they consider an indicator of strong miner confidence.

The report states that miners are bullish on Bitcoin and are committing more resources to mining, leading to increased mining difficulty. However, they are also hedging their position by dispatching more Bitcoin to exchanges.

The report suggests that miners are hedging their positions on derivatives exchanges, with 70,000 BTC transferred in the first week of July 2023.

This volume of transfers to exchanges is considered rare and potentially showcases new miner behavior.

Bitfinex also mentions data from Glassnode, indicating that Poolin has been responsible for a significant portion of this activity, offloading BTC to Binance.

The report discusses various plausible reasons behind this mining behavior, including hedging activities in the derivatives market, carrying out over-the-counter orders, or transferring funds through exchanges for other purposes.

READ MORE: Celo Blockchain Plans Transition to Ethereum Layer-2 Solution

The increase in mining difficulty suggests the addition of new mining power to the Bitcoin network.

Analysts interpret this as a sign of improved network health and increased confidence in mining profitability, driven by higher BTC prices or improved hardware.

Additionally, the report suggests that on-chain Bitcoin movements reflect a transfer of supply from long-term holders to short-term holders.

This behavior is commonly observed during bull market conditions, with new market traders seeking quick profits while long-term holders capitalize on increased prices.

To shed light on the increase in Bitcoin outflows from miners in the past month, Cointelegraph has reached out to several mining companies and pools for clarification.

In June 2023, miners sent over $128 million in revenue to exchanges, as reported previously.

Other Stories:

SEC Chair Gary Gensler Advocates Greater Use of Artificial Intelligence for Market Surveillance

PEPE Coin in Trouble? Financial Regulator Clamps Down On Crypto Memes

FSB Proposes Global Regulatory Framework for Cryptocurrencies

Bitcoin (BTC) experienced a drop below the $30,000 mark on July 18, surprising retail investors who had witnessed positive developments in the past month.

However, this downward movement does not indicate a shift in the long-term trend.

Despite the recent decline, there are positive signs to consider. Bitcoin is still making efforts to establish $30,000 as a support level, with numerous attempts since April.

Moreover, buyers consistently emerge within the $28,000 to $25,000 range, which seems to be viewed as an accumulation zone.

Glassnode’s Bitcoin Accumulation Trend Score aligns with this sentiment, revealing that larger entities are accumulating BTC rather than distributing it.

The Accumulation Trend Score indicates that buyers were accumulating from November to December and continued to do so from March to April when Bitcoin surpassed $30,000.

The score suggests that the same accumulation behavior is occurring in July, possibly due to Bitcoin’s attempt to conquer the $30,000 resistance or the positive news surrounding ETFs and XRP SEC.

The current price action and derivatives market data indicate that Bitcoin is in a crab market, characterized by a range-bound price that consolidates for an extended period.

Breaking through the $32,000 level could trigger a CME gap fill from the Luna Terra-crash era.

On a weekly market structure basis, $30,000 serves as a crucial pivot point, previously functioning as support in the last bull market cycle and now as resistance.

READ MORE: Celo Blockchain Plans Transition to Ethereum Layer-2 Solution

Surpassing this level would signify a higher high and confirm a trend reversal, with the next resistance point at approximately $37,000.

In the derivatives market, trading activity remains relatively muted, with funding down and open interest not displaying significant surges.

This suggests that a substantial breakout is yet to occur. While the recent dip in the DXY (U.S. Dollar Currency Index) may have influenced investor sentiment, it is unlikely to trigger an immediate massive reaction in Bitcoin.

Although short-term price fluctuations may concern new investors and day-traders, the on-chain perspective presents a compelling outlook.

The Total Balance in Accumulation Addresses metric has been on an uptrend since March 16, indicating that investors continue to increase their allocation to Bitcoin, even throughout the crypto market collapse and price sell-off.

It is worth noting that the metric also reveals a continuous increase in the total balance in accumulation addresses since January 2022, when Bitcoin was trading at $47,800 per coin.

This data highlights investors’ long-term confidence in Bitcoin and their ongoing accumulation of the cryptocurrency.

Other Stories:

PEPE Coin in Trouble? Financial Regulator Clamps Down On Crypto Memes

SEC Chair Gary Gensler Advocates Greater Use of Artificial Intelligence for Market Surveillance

FSB Proposes Global Regulatory Framework for Cryptocurrencies

The dYdX Foundation, a non-profit organization dedicated to supporting the dYdX protocol in decentralized finance (DeFi), has announced the launch of a public testnet for its latest version, v4.

This achievement has put dYdX ahead of schedule for the anticipated release of the v4 mainnet, marking a significant milestone towards complete decentralization for the platform.

As outlined in its roadmap towards decentralization, the recent testnet launch represents the fourth out of five milestones set by dYdX.

Currently, the live version of dYdX is considered partially centralized, utilizing a centralized order book and matching system while not holding custody of user assets.

The forthcoming v4 version is expected to resolve this issue and achieve full decentralization.

dYdX is currently the world’s largest decentralized exchange for perpetuals, which are bonds without a maturity date, facilitating over $1 billion in daily fund transfers.

Charles d’Haussy, CEO of the dYdX Foundation, discussed the move towards complete decentralization and its impact on centralized providers of perpetuals.

READ MORE: PEPE Coin in Trouble? Financial Regulator Clamps Down On Crypto Memes

According to d’Haussy, centralized providers are not direct competitors to the dYdX protocol, as they have played a crucial role in supporting the market, with BitMex being credited as the originator of perpetuals.

He views the industry as transitioning towards a state of “decentralized disruption,” but emphasizes that centralized organizations can coexist and collaborate with DeFi platforms, benefiting the broader crypto community.

D’Haussy envisions a future where centralized exchanges serve as gateways to decentralized exchanges, offering customers an enhanced experience and seamless integration.

Drawing a parallel with traditional financial institutions, he suggests that banks often provide additional services alongside their core business.

He believes this model can be applied to crypto, as long as it empowers users to adopt crypto services in ways that suit their preferences.

The CEO views this as a positive development for the ecosystem, emphasizing that people have diverse consumption preferences.

If a centralized entity can provide a more accessible and comfortable means of managing crypto assets, while also facilitating access to DeFi, it would be beneficial for users.

In conclusion, the dYdX Foundation’s launch of the v4 testnet has propelled the platform closer to achieving complete decentralization.

The CEO’s perspective highlights the potential for collaboration between centralized and decentralized providers, with centralized exchanges serving as gateways to DeFi, offering users a seamless and personalized crypto experience.

Other Stories:

FSB Proposes Global Regulatory Framework for Cryptocurrencies

Celo Blockchain Plans Transition to Ethereum Layer-2 Solution

SEC Chair Gary Gensler Advocates Greater Use of Artificial Intelligence for Market Surveillance

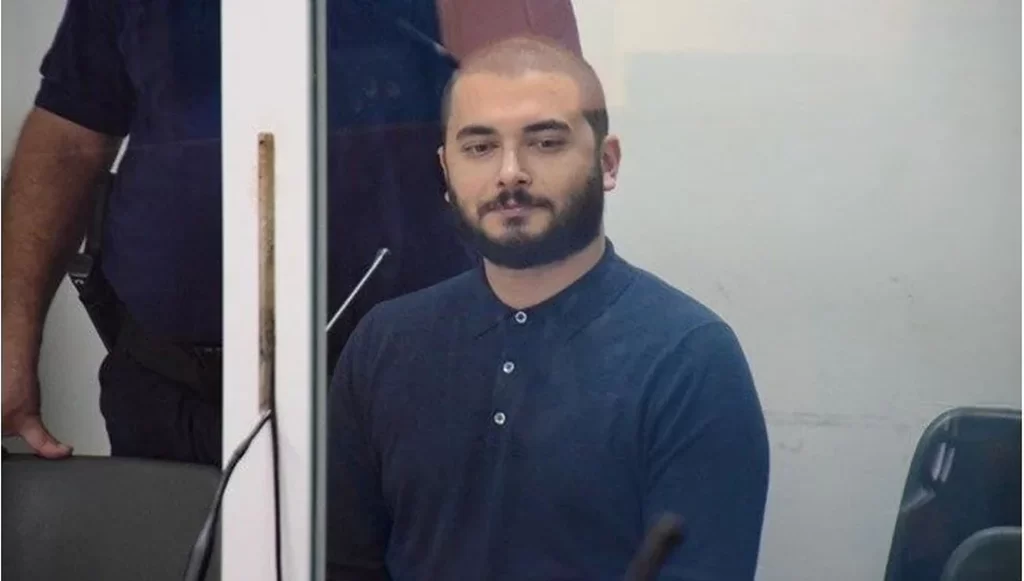

Founder and former CEO of Thodex, Faruk Fatih Özer, has been sentenced to seven months and 15 days in prison for his failure to submit requested documents during his trial.

Özer, who had previously been detained and later fled to Albania, was apprehended and deported back to Türkiye following a Red Notice by Interpol.

The closure of Thodex, once a prominent cryptocurrency exchange in the country, left investors with approximately $2 billion worth of cryptocurrencies.

Throughout the trial, Özer maintained his innocence but failed to provide the requested documents to the Tax Inspection Board.

He argued that he was not the official representative of Thodex during the specified period and therefore could not present the requested books.

Özer claimed that a trustee had been appointed to manage the business on his behalf during that time.

Initially, Özer’s prosecutor sought a five-year prison sentence for “smuggling” under the Tax Procedure Law.

However, the court initially sentenced him to one year and six months, which was later reduced to seven months and 15 days.

The reduction was based on factors such as Özer’s social relations, overall behavior, and conduct during the trial.

READ MORE: Web3 Needs Asset Protection, and This Startup Wants to Make it Widely Available

Apart from tax-related charges, Özer also faces accusations of defrauding Thodex investors, and a hearing on these claims is pending.

Despite the allegations, Özer maintains his innocence and asserts that he has been framed by the defendants.

In a related context, a recent study by Swedish crypto tax firm Divly revealed that a vast majority of crypto investors, approximately 99.5%, did not pay taxes in 2022.

The report highlighted that Finland had the highest proportion of crypto investors who fulfilled their tax obligations at 4.09%, closely followed by Australia at 3.65%.

However, the report acknowledged the questionable methodology used to derive these estimates, emphasizing that search volume data might not accurately reflect the actual number of crypto taxpayers, as not all individuals who pay taxes search for crypto tax-related information online.

As the legal proceedings continue, the case of Faruk Fatih Özer and Thodex serves as a reminder of the complexities surrounding cryptocurrency regulation and taxation.

It underscores the importance of transparency and accountability in the crypto industry and highlights the need for robust regulatory frameworks to protect investors and ensure the integrity of digital asset exchanges.

Other Stories:

Ex-Federal Prosecutor Surprised by Potential SEC Appeal in Ripple Case

3 Best Crypto PR Agencies – Fees, Results and Full Review

Bitcoin On-Chain Data Reveals $30,000 as Most Popular ‘Buy’ Level